In other words profits of the competitive firm are in the long run maximum at the level of output at which long-run average cost is minimum. Whether the goods offered are identical or differentiated 3.

Long Run Equilibrium Under Perfect Competition Ii

A perfectly competitive firm is known as a price taker because the pressure of competing firms forces it to accept the prevailing equilibrium price in the market.

. The firms in the long run can increase their output by changing their capital equipment. The long-run equilibrium quantity in a perfectly competitive structure is. The number of firms in the market one few or many 2.

Short-run average total cost and long-run average cost are at a minimum. If a firm in a perfectly competitive market raises the price of its product by so much as a penny it will lose all of its sales to competitors. Perfect competition many firms each selling an identical standardized product and no barriers to.

What is long run equilibrium in perfect competition. In the long run all factors are variable and none fixed. Monopolists create a contrived scarcity by producing an output below the perfectly competitive equilibrium output long run profit short run profit.

Short Run and Long Run Equilibrium under Perfect Competition with diagram. Barriers to entry Four types of market structure. Long-run Equilibrium Under Each Market Structure A firm is said to be at equilibrium if the marginal cost MC is equal to marginal revenue MR and that is the profit-maximizing level of output.

Types of Market Structure We can distinguish types of market structures by focusing on three features. There is no incentive for firms to leave the industry or for new firms to enter it. When a wheat grower as we discussed.

It produces a quantity depending upon its cost structure. In long-run equilibrium a competitive firm produces the level of output at which. Long-run equilibrium in perfect competition In the long-run firms can make the necessary adjustment to their capacity.

At the equilibrium quantity if the average cost is equal to the average revenue then the firm is earning a normal profit. The conclusion is that at equilibrium in the long run a monopoly would sell a smaller quantity and at a higher price than if the market structure was perfect competition. See also Can Target Price Match Amazon Prime.

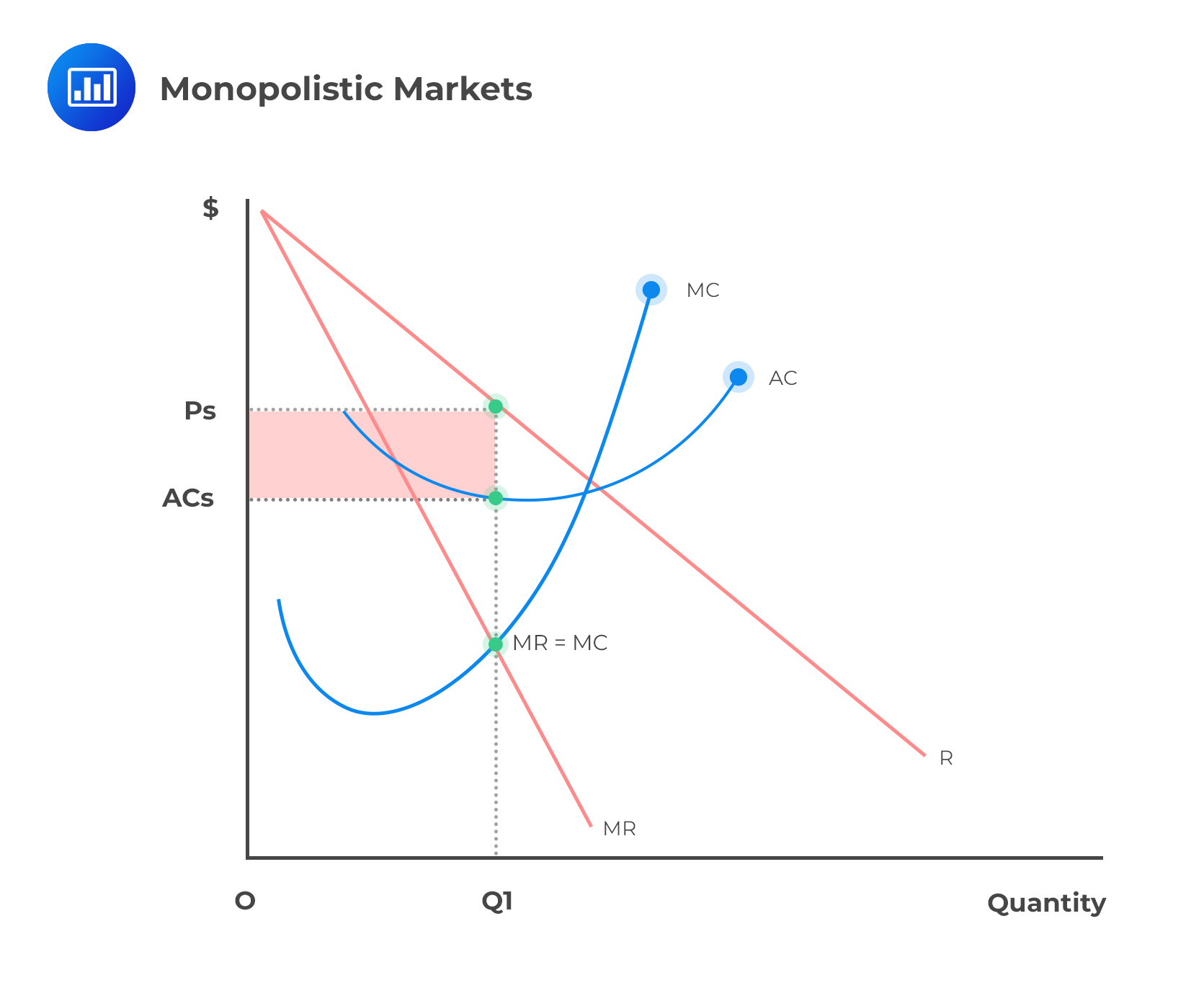

In long-run equilibrium under perfect competition the price of the product becomes equal to the minimum long-run average cost LAC of the firm. In the long-run economic profit cannot be sustained. The long-run equilibrium point for a perfectly competitive market occurs where the demand curve price intersects the marginal cost MC curve and the minimum point of the average cost AC curve.

The long-run equilibrium point for a perfectly competitive market occurs where the demand curve price intersects the marginal cost MC curve and the minimum point of the average cost AC curve. For better understanding If separate diagrams are required to answer the question. The long run is a period of time which is sufficiently long to allow the firms to make changes in all factors of production.

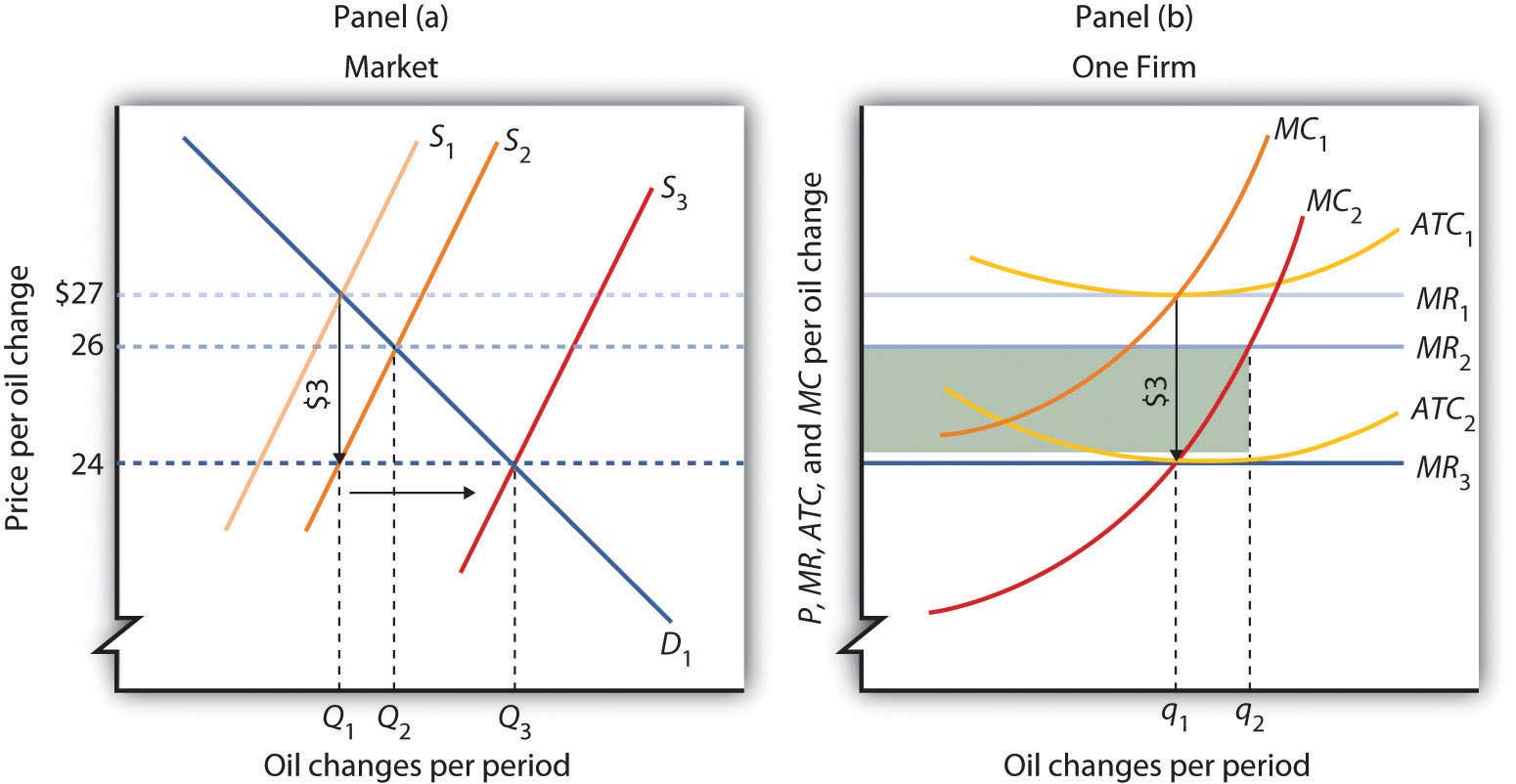

The diagram below shows only the perfect competitor in long-run equilibrium. In monopoly on the other hand long- run equilibrium occurs at the point of intersection between the monopolists marginal revenue MR and long-run marginal cost LMC curves. The cost to society of producing the marginal units.

Average Total Cost Marginal Cost Market Price A firm maximizes profit when its marginal revenue MR equals its marginal cost MC equals the average total cost ATC. The Long-Run Equilibrium of the Firm under Perfect Competition. Select all that apply.

Perfect Competition in the Long Run. The long-run equilibrium point for a perfectly competitive market occurs where the demand curve price intersects the marginal cost MC curve and the minimum point of the average cost AC curve. Accordingly they will adjust their capacity to produce at the minimum point of the long-run average cost LAC curve which is tangent to the demand curve defined by the market price.

The existence of economic profits attracts entry economic losses lead to exit and in long-run equilibrium firms in a perfectly competitive industry will earn zero economic profit. The monopolistically competitive firms longrun equilibrium situation is illustrated in Figure. On the other hand if the average cost is greater than the average revenue then the firm is bearing a loss.

The industry under perfect competition is defined as all the firms taken together. In monopoly on the other hand long- run equilibrium occurs at the point of intersection between the monopolists marginal revenue MR and long-run marginal cost LMC curves. Long-run equilibrium in perfect competition In the long-run firms can make the necessary adjustment to their capacity.

In the long-run economic profit cannot be sustained. Assume a market in a long run competitive equilibrium experiences a decrease in demand. They may expand their old plants or replace the old.

In a perfectly competitive market a firm can earn a normal profit super-normal profit or it can bear a loss. Marginal cost is at a minimum. In the long-run economic profit cannot be sustained.

Fourth important difference between the two is that while the perfectly. The entry of new firms leads to an increase in the supply of differentiated products which causes the firms market demand curve to shift to the left. Perfect Competition in the Long Run.

All of the answers above are correct. And since suppliers will produce until marginal cost market price the long-run equilibrium in a purely competitive market can be summarized thus. The industry is in equilibrium in the long run when all firms earn normal profits.

The long-run supply curve in an industry in which expansion does not change input prices a constant-cost industry is a horizontal line. Perfect Competition in the Long Run. Long-Run Equilibrium of the Perfectly Competitive Industry.

Under perfect competition price determination takes place at the level of industry while firm behaves as a price taker. In long-run equilibrium under perfect competition the price of the product becomes equal to the minimum long-run average cost LAC of the firm. After market adjustments occur what is the net change in market price and quantity after the market returns to a long run equilibrium.

Accordingly they will adjust their capacity to produce at the minimum point of the long-run average cost LAC curve which is tangent to the demand curve defined by the market price. On the other hand in case of the competitive firm marginal revenue or price in long-run equilibrium is equal to both marginal cost and minimum average cost.

Pure Competition Long Run Equilibrium

Perfect Competition In The Long Run

Long Run Equilibrium Under Each Market Structure Analystprep Cfa Exam Study Notes

0 Comments